Application Process

A complete guide to approaching M&A case studies at law firm assessment centres, with a full worked example using a real case study from a future trainee solicitor at a US firm.

EO Careers Team

If you are preparing for a law firm assessment centre, our Application Process hub covers every stage of the recruitment process from written applications and psychometric tests through to interviews and offers.

M&A case studies are one of the most commonly used exercises at law firm assessment centres, and one of the exercises candidates find hardest to prepare for. Unlike competency interviews or commercial awareness questions, case studies require you to apply legal and commercial thinking simultaneously, under time pressure, to a set of facts you have never seen before. The candidates who perform best are not necessarily those with the most legal knowledge. They are those who have a clear analytical framework, understand what the exercise is actually testing, and have practised enough to recognise the issue types that appear consistently across different case studies.

This guide covers how to approach M&A case studies from first principles, what the structure of a strong answer looks like, and then walks through every issue in a real case study in full, using the framework that helped a future trainee solicitor at a US firm secure his training contract in his second year of university.

What case studies are testing

Before looking at structure or issue spotting, it is worth understanding what the assessors are looking for, because it changes how you approach the exercise.

A case study at a law firm assessment centre is not primarily a test of legal knowledge. It is a test of how you think under pressure and whether you can apply commercial and legal reasoning to a realistic scenario in a structured, client-focused way. The assessors are looking for three things above all others.

The first is issue spotting: can you identify the legally and commercially significant problems in the fact pattern? Some issues will be obvious. Others will require you to read carefully, notice what is implied rather than stated, and ask the right questions about what you have been told.

The second is commercial understanding: do you understand how each issue actually affects the client? Identifying that there is a competition law concern is not enough. Explaining why it matters to SuperComputers, what it could mean for the transaction, and what the client needs to do about it is what earns marks.

The third is practical legal advice: can you identify which teams at the law firm would be involved, what mechanisms are available, and what the options are including their trade-offs? Firms are not looking for a single correct answer. They are looking for evidence that you can think like an advisor rather than a student.

The structure that works

Before reading a single word of the case study itself, internalise this four-step framework. It applies to every issue you identify and gives your answer a consistent structure that is easy to follow and easy to score.

Step 1: Identify the issue. What is the problem? State it clearly and specifically. Not "there might be competition concerns" but "the scale of Chippy Ltd as a mega business with global market presence raises potential competition and antitrust concerns that could prevent the transaction completing."

Step 2: Explain why it matters to the client. How does this issue affect SuperComputers' ability to complete the acquisition, or the value of what they are acquiring? This is where most candidates lose marks. Spotting the issue is the beginning, not the answer.

Step 3: Identify how the law firm can help. Which practice group or team at the firm would advise on this? Where you can, be specific about the firm you are applying to. If the firm has a dedicated data privacy team or a well-known competition practice, reference it. Generic references to "a team at the firm" are weaker than firm-specific ones.

Step 4: Offer multiple solutions and evaluate them. Do not give a single recommendation. Identify two or more possible approaches, explain the advantages and disadvantages of each, and indicate which you would recommend and why. This demonstrates the kind of balanced, advisory thinking that commercial lawyers apply in practice.

One final point on structure before the walkthrough: summarise the case study briefly at the start before going into the issues, but keep it short. State what the transaction is, why it makes commercial sense (the synergies), and that there are several issues to work through. Do not summarise the issues themselves in the introduction. You are going to cover each one in full. Summarising them twice wastes time and weakens the structure.

The case study

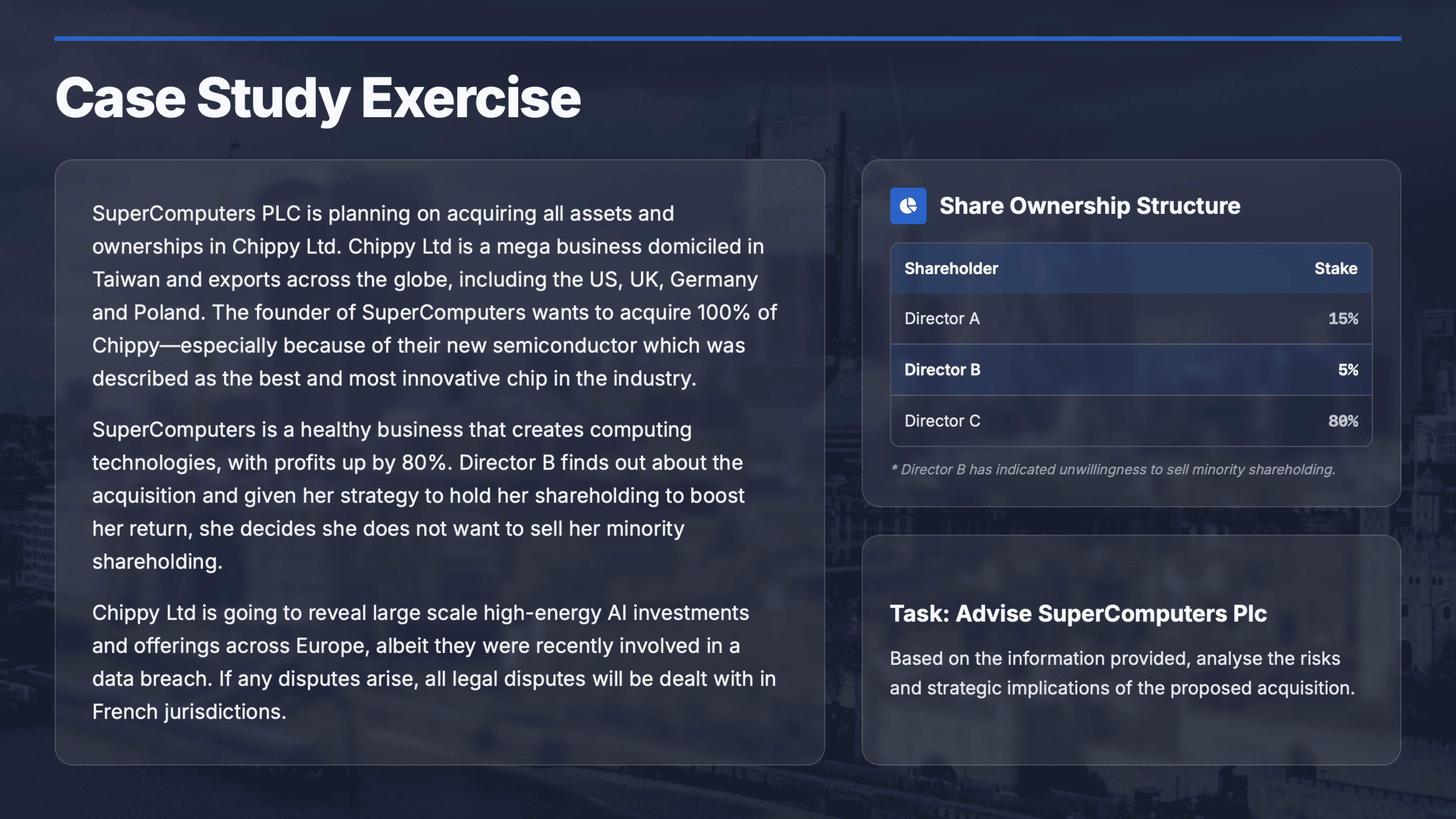

SuperComputers PLC is planning to acquire all assets and ownership in Chippy Ltd. Chippy Ltd is a mega business domiciled in Taiwan and exports across the globe, including the US, UK, Germany, and Poland. The founder of SuperComputers wants to acquire 100% of Chippy, particularly because of their new semiconductor described as the best and most innovative chip in the industry.

SuperComputers is a healthy business that creates computing technologies, with profits up by 80%. Director B finds out about the acquisition and given her strategy to hold her shareholding to boost her return, she decides she does not want to sell her minority shareholding.

Chippy Ltd is going to reveal large scale high-energy AI investments and offerings across Europe, albeit they were recently involved in a data breach. If any disputes arise, all legal disputes will be dealt with in French jurisdictions.

Share ownership structure:

Shareholder | Stake |

|---|---|

Director A | 15% |

Director B | 5% |

Director C | 80% |

Director B has indicated unwillingness to sell her minority shareholding.

Task: Based on the information provided, analyse the risks and strategic implications of the proposed acquisition, and advise SuperComputers PLC.

Summary of the transaction

This is a share purchase rather than an asset purchase. SuperComputers wants 100% ownership of Chippy Ltd, which means acquiring all shares including the minority stake held by Director B. A share purchase gives the acquirer full control and ownership of the company, including all of its assets, liabilities, and contracts. It requires more thorough due diligence than an asset purchase because you are acquiring everything, not cherry-picking specific assets, but it gives SuperComputers the control they need to direct the business going forward.

The commercial rationale is clear. SuperComputers creates computing technologies and has seen profits rise 80%. Chippy Ltd produces what has been described as the most innovative semiconductor currently in the market. The synergy is direct: a superior semiconductor enhances computing performance, which strengthens SuperComputers' core product offering and competitive position. The acquisition makes commercial sense, which is why the transaction is proceeding.

There are several significant legal and commercial issues that need to be addressed before, during, and after completion. They are worked through below in the order a lawyer advising on this transaction would typically consider them.

Issue 1: Competition and antitrust concerns

The issue. Chippy Ltd is described as a mega business. The fact pattern does not define this further, but the term signals significant market presence. When a large company acquires another large company, regulators will scrutinise whether the combined entity creates an unfair advantage, reduces competition, or gives the acquirer the kind of market power that harms other competitors or consumers.

Why it matters to the client. The Competition and Markets Authority in the UK, the European Commission for EU matters, and equivalent regulators in the US and other jurisdictions where Chippy operates will each have the authority to review and potentially prohibit this transaction if it creates a dominant market position. SuperComputers cannot complete the acquisition, or may be forced to unwind it, if regulatory clearance is not obtained. For a transaction of this scale and strategic importance, this is one of the most significant procedural risks.

How the law firm can help. The competition and antitrust team at the firm will assess whether the transaction crosses the notification thresholds in each relevant jurisdiction, prepare the necessary merger filings, manage the regulatory review process, and advise on any remedies the regulators might require (such as divesting a part of the business) as a condition of approval. The competition team will also advise on the timing implications, since regulatory review can take months and affects the overall transaction timeline.

Solutions and trade-offs. The most important practical tool here is a conditions precedent clause in the transaction documentation. A conditions precedent provision states that the transaction will not complete unless specific conditions are satisfied, in this case regulatory approval from the relevant authorities. Without this provision, SuperComputers could transfer consideration only to find that the regulator subsequently blocks or unwinds the deal. Including a conditions precedent clause protects the client against this outcome.

The trade-off is that conditions precedent introduce uncertainty into the timeline. SuperComputers should be prepared for the possibility that the regulatory process takes longer than anticipated, particularly given Chippy's presence across multiple jurisdictions including the US, UK, and EU, each of which may require separate filings.

Issue 2: Intellectual property protection

The issue. The transaction is motivated in large part by Chippy's semiconductor, described as the most innovative chip in the industry. The question the lawyers need to answer immediately is whether that semiconductor is adequately protected under intellectual property law, specifically whether a patent has been granted for the invention.

Why it matters to the client. If the semiconductor is not protected, competitors can replicate it. The primary commercial justification for the acquisition is eroded the moment other chip manufacturers can produce an equivalent product. SuperComputers needs to understand the IP position before committing to the transaction, because the value they are paying for is heavily dependent on the exclusivity of the technology.

How the law firm can help. The IP team will conduct a thorough IP audit as part of due diligence. They will check whether a patent has been granted and, if so, its scope, duration, and the jurisdictions it covers. If no patent has been filed, the IP team will assess whether Chippy has sufficient documentation to establish inventorship and file for protection, and whether the semiconductor qualifies for patent protection in the relevant markets.

Solutions and trade-offs. If a patent exists and is valid, the primary task is ensuring the IP rights transfer correctly as part of the share purchase. If a patent does not exist, there are two options. The first is to proceed with the acquisition while simultaneously filing for patent protection, accepting that there is a window of vulnerability during which competitors could attempt to replicate the technology. The second is to make the acquisition conditional on obtaining adequate IP protection, which reduces the client's risk but introduces further delay. The right approach depends on the competitive landscape and how quickly a competitor could realistically reverse-engineer the semiconductor.

IP issues are almost always present in M&A case studies involving technology companies. If the fact pattern does not mention IP explicitly, it is still worth flagging that the IP position needs to be investigated as part of due diligence.

Issue 3: Director B's refusal to sell her minority shareholding

The issue. Director B holds 5% of Chippy Ltd and has indicated she does not want to sell. SuperComputers wants 100% ownership. This creates a direct obstacle to completing the transaction on the terms required.

Why it matters to the client. SuperComputers' stated objective is full ownership of the company. Acquiring 95% does not achieve this, and depending on how the shareholders' agreement is structured, a minority shareholder retaining their stake can complicate governance, create future disputes, and in some circumstances give the minority shareholder rights that constrain how the majority owner operates the business.

Director B's reasoning matters too. She is holding her stake because she believes it will generate better returns in the future. This is a financial calculation, not a strategic objection to the acquisition itself. That distinction is important because it suggests a financial solution may be available.

How the law firm can help. The employment and incentives team at the firm will be involved in structuring any package designed to incentivise Director B to sell. The corporate team will advise on whether a drag along right exists in the shareholders' agreement and how it would operate.

Solutions and trade-offs.

The first option is a negotiated package. If Director B's concern is the return she expects from holding her shares, the acquiring company can offer her a deal that meets or exceeds that expected return: a premium on the share price, a retention bonus, an enhanced employment package, or some combination of these. This is almost always the better option where the relationship can be preserved, because it achieves the acquisition objective while maintaining a relationship with a senior figure who has deep knowledge of the business.

The second option is to enforce a drag along right, if one exists in the shareholders' agreement. A drag along right allows the majority shareholder to compel the minority to sell their shares on the same terms when a sale of the majority stake is agreed. In this transaction, Director C holds 80% and Directors A and C together hold 95%. If the shareholders' agreement contains a drag along right triggered at majority level, Director B can be compelled to sell at the same price agreed for the majority stake.

There are two important caveats. First, the drag along right must actually exist in the shareholders' agreement. The fact pattern does not confirm this, and the lawyers need to check before advising on it. Second, even if it exists, forcing a director out of the business creates reputational and relationship consequences. If Director B has expertise, client relationships, or institutional knowledge that is valuable to the acquiring business, compelling her departure through a legal mechanism rather than a negotiated exit may damage the very assets SuperComputers is trying to acquire.

The recommended approach is to attempt a negotiated package first. If that fails, assess whether a drag along right exists and whether enforcing it is proportionate given the wider relationship implications.

Issue 4: EU AI Act compliance

The issue. Chippy Ltd is planning to reveal large scale AI investments and offerings across Europe. The EU AI Act, which came into force in 2024 and is being implemented in stages through 2026 and beyond, creates a binding regulatory framework for AI products and services operating in the EU. AI systems are classified into risk categories, with different compliance obligations depending on the category.

Why it matters to the client. If Chippy's AI offerings are not compliant with the EU AI Act at the point of acquisition, SuperComputers inherits that non-compliance. The penalties for breaching the EU AI Act are significant, reaching up to 35 million euros or 7% of global annual turnover for the most serious violations. For a business with Chippy's scale and international presence, this is a material financial and reputational risk.

How the law firm can help. The regulatory compliance team at the firm will assess whether Chippy's existing and planned AI offerings fall into the high-risk, limited-risk, or minimal-risk categories under the EU AI Act, what compliance obligations attach to each category, and whether those obligations have been met. If there are gaps, the team will advise on what needs to be implemented before the acquisition completes or immediately after.

Solutions and trade-offs. The lawyers should recommend that a regulatory compliance audit of Chippy's AI systems forms part of pre-acquisition due diligence. If material non-compliance is identified, SuperComputers has three options: require Chippy to achieve compliance before completion as a condition of the transaction, negotiate a price reduction to reflect the cost and risk of achieving compliance post-acquisition, or include an indemnity in the transaction documents requiring the sellers to compensate SuperComputers for any losses arising from pre-completion non-compliance.

The EU AI Act's requirements are evolving, which makes this an area where specialist regulatory advice is essential rather than optional.

Issue 5: The data breach

The issue. The fact pattern states that Chippy Ltd was recently involved in a data breach. This is a serious issue that needs to be understood in detail before the transaction completes.

Why it matters to the client. A data breach can expose a company to regulatory sanctions under GDPR and equivalent data protection laws in other jurisdictions, civil claims from individuals whose data was affected, reputational damage, and ongoing operational costs of remediation. For a technology company whose product offering depends in part on trust and data security, a significant data breach can affect both the value of the business and its future regulatory standing. SuperComputers needs to understand what happened, how serious it was, whether it has been properly reported to the relevant data protection authorities, and what the residual liability is.

How the law firm can help. Three teams are likely to be involved. The investigations team will conduct a forensic investigation into what data was compromised, how the breach occurred, and whether similar breaches are likely in the future. The data privacy team will assess the company's compliance with its notification obligations under GDPR (which requires notification to the relevant supervisory authority within 72 hours of becoming aware of a breach) and advise on the regulatory exposure. The litigation team will assess any pending or likely civil claims.

Solutions and trade-offs. The first priority is understanding the full extent of the breach and whether all regulatory obligations have been met. If notification has not been made where required, this needs to be rectified immediately because the penalties for failing to notify are separate from and additional to the penalties for the breach itself.

Beyond this, the transaction documents should include a specific indemnity from the sellers covering any losses, claims, or regulatory sanctions arising from the data breach that occur after completion but relate to pre-completion events. An indemnity provides pound-for-pound compensation for covered losses, giving SuperComputers direct financial protection against a risk that it has not created but will inherit.

SuperComputers should also consider whether the data breach affects the transaction valuation. If the reputational damage to Chippy's brand is material, or if the remediation costs are significant, this should be reflected in the price.

Issue 6: Jurisdiction clause

The issue. The fact pattern states that all legal disputes arising from the transaction will be dealt with in French jurisdictions. SuperComputers is a UK company.

Why it matters to the client. A jurisdiction clause determines where disputes must be litigated and which country's law governs the resolution. Requiring a UK company to litigate all disputes in France creates significant practical burdens: additional cost, the need for French legal representation, and a system of law that may be less familiar to SuperComputers' lawyers and advisors. English law and the English courts are internationally respected and are the preferred choice for most commercial transactions involving UK parties. English courts also have extensive experience with complex commercial disputes arising from M&A transactions.

How the law firm can help. The corporate team, potentially alongside the disputes team if there are existing proceedings, will advise on renegotiating the jurisdiction clause before the transaction documents are finalised. This is the kind of provision that can often be changed in negotiation without significant difficulty, particularly where the other side has no strong reason to insist on French jurisdiction other than historical habit or oversight.

Solutions and trade-offs. The recommended approach is to negotiate the jurisdiction clause to provide for English law and the exclusive jurisdiction of the English courts. Where the transaction has genuinely multi-jurisdictional dimensions, a tiered approach can be considered: English jurisdiction for the core transaction documents, with specific carve-outs for disputes that genuinely relate to assets or operations in a particular jurisdiction. However, the simpler the jurisdiction structure, the easier it is to manage if a dispute arises.

Issue 7: ESG and high-energy AI operations

The issue. The fact pattern describes Chippy's AI investments as high-energy. This is a potential ESG concern because AI data centres are significant consumers of electricity and water, and regulators, investors, and consumers are increasingly focused on the environmental footprint of technology companies.

Why it matters to the client. If SuperComputers has its own ESG commitments or targets, acquiring a business with high-energy AI operations could create a conflict between those commitments and the operations of the combined entity. There is also a regulatory dimension: the EU Taxonomy Regulation and related ESG reporting obligations require large companies to disclose whether their activities are environmentally sustainable, and a high-energy operation may be difficult to classify as sustainable under current criteria.

How the law firm can help. The ESG team and the energy regulatory team will assess whether Chippy's AI operations are compliant with applicable energy and environmental regulations, whether they are consistent with SuperComputers' existing ESG reporting obligations, and whether any remediation or transition planning is required post-acquisition.

This issue may not always be flagged by candidates, but the ability to identify an implied ESG concern from a single descriptor like "high-energy" demonstrates exactly the kind of careful reading and commercial awareness that assessors are looking for.

Issue 8: Geopolitical risk — Taiwan domicile and semiconductor supply chain

The issue. Chippy Ltd is domiciled in Taiwan. Taiwan is the world's leading producer of advanced semiconductors, but it faces a specific combination of geopolitical risks that are directly relevant to this transaction: ongoing tensions with China, which claims Taiwan as its territory; US-China trade tensions and semiconductor-related export controls; water scarcity affecting semiconductor manufacturing; and potential labour market pressures.

Why it matters to the client. The value of the acquisition depends significantly on Chippy's continued ability to manufacture and export its semiconductors. If geopolitical escalation, sanctions, or supply chain disruption were to affect Chippy's manufacturing capacity, SuperComputers' core rationale for the acquisition could be undermined. The US has imposed export controls on advanced semiconductor technology, and further restrictions could affect Chippy's ability to operate in certain markets. China has indicated ambitions to develop domestic semiconductor capability, which could create competitive pressure over the medium term.

How the law firm can help. A conflicts and sanctions team will assess whether any existing or anticipated sanctions regimes affect Chippy's operations or the transaction itself. The corporate team will advise on how geopolitical risk can be addressed in the transaction documents, for example through material adverse change clauses that allow the buyer to withdraw if a defined geopolitical event occurs before completion.

Solutions and trade-offs. SuperComputers should commission a geopolitical risk assessment as part of due diligence. The transaction documents should include a well-drafted material adverse change clause that captures geopolitical events affecting Chippy's manufacturing operations or export capacity. The buyer should also consider whether diversifying Chippy's manufacturing base away from Taiwan over time is a strategic priority post-acquisition.

Issue 9: Financial health and deal financing

The issue. The fact pattern tells us SuperComputers is a healthy business with profits up 80%. This sounds positive, but a lawyer advising on the transaction needs to probe what this means in practice.

Why it matters to the client. Revenue growth and profit growth are different things. A company can have high revenue and modest profits if its cost base is growing faster than its income. Profits up 80% from a small base may still represent a modest absolute figure. The finance team needs to understand whether SuperComputers has the capital to fund this acquisition, whether it will need to raise debt or equity financing, and whether the acquisition makes financial sense given the total consideration, including contingent liabilities inherited from Chippy.

How the law firm can help. The finance team will advise on the optimal financing structure for the acquisition. If SuperComputers is using retained profits, the team will ensure the corporate mechanics are correctly handled. If external financing is required, the banking and finance team will advise on the available structures, including term loans, revolving credit facilities, and hybrid instruments.

The tax team will also be involved to ensure the transaction is structured in a way that is tax efficient across all relevant jurisdictions, including the UK, Taiwan, the US, Germany, and Poland.

Other teams that may be involved

Depending on what emerges during due diligence, additional practice groups may need to be engaged:

Real estate: If Chippy Ltd owns property, the real estate team will investigate title, check for third party interests, and ensure the properties transfer cleanly as part of the acquisition.

Employment: Beyond the Director B situation, the employment team will review Chippy's employment contracts, particularly for key personnel whose departure could affect business value, and advise on any TUPE-equivalent obligations in the relevant jurisdictions.

Compliance: The compliance team will assess whether Chippy is internally compliant with the legal and regulatory obligations applicable to its business across all jurisdictions, including employment law, health and safety, and sector-specific regulations.

How to present your findings

After the case study analysis, you will often be asked to present your findings. For guidance on the presentation element, see our presentations guide.

When presenting a case study at an assessment centre, either in writing or verbally, the structure that works is the same regardless of the exercise format. Begin with a brief summary of the transaction and its commercial logic. Work through each issue using the four-step framework (identify, explain impact on client, identify firm involvement, evaluate options). Close with an overall recommendation that draws together the key risks and the conditions under which you would advise the client to proceed.

The candidates who perform best in case studies are those who demonstrate that they are thinking like an advisor rather than a student. That means connecting every legal observation to a commercial consequence, offering a view on the options rather than just listing them, and showing that you understand what the client is actually trying to achieve and why each issue might threaten or affect that goal.

Practise is essential. The more case studies you work through, the more familiar the issue types become and the more efficiently you can spot them in a new fact pattern. Many of the issues in this case study, competition concerns, IP protection, minority shareholder disputes, data breaches, jurisdiction clauses, ESG considerations, appear repeatedly across different case studies in different forms.

Case studies are typically combined with group exercises and a presentation on the same assessment day. For a full guide to the group exercise, see our group exercises guide.

Want to practise with real assessment centre exercises?

The Future Trainee Academy includes worked case study examples and guidance from trainees who have been through the assessment centre process at leading firms, covering how to structure your analysis, how to present under time pressure, and how to demonstrate commercial awareness throughout. Free to access.

For broader interview and assessment centre preparation including competency questions, commercial awareness, and situational judgment, see the Interview Question Bank.